Mercer released the results of its 13th Annual Mercer CFA Institute Global Pension Index (MCGPI) which for the first time included the United Arab Emirates (UAE). The UAE’s retirement income system ranked 22nd among countries with long-standing pension systems such as United States of America, France and Spain. Globally, Iceland ranked number one followed by the Netherlands, while Thailand ranked last.

The MCGPI is a comprehensive study of global pension systems, accounting for two-thirds (65 per cent) of the world’s population. It benchmarks retirement income systems around the world highlighting some shortcomings in each system and suggests possible areas of reform that would provide more adequate and sustainable retirement benefits. The UAE system scored among global peers across three key areas of focus: adequacy, sustainability and integrity.

Within the UAE, pensions of Emiratis are governed by different agencies such as the Abu Dhabi Pension Fund (ADPF), Sharjah Social Security Fund (SSSF) and the General Pensions and Social Security Authority (GPSSA). The UAE’s pension adequacy rankings are supported by country’s generous retirement benefits, which ensure a continued income to sustain a good quality of life with a suitable minimum pension relative to earnings.

The UAE also scored well in terms of sustainability given its high labor force participation rate, especially for individuals over the age of 55. In fact, the retirement income system in the UAE enacts a sound structure to develop a funded pension system for Emiratis with both the public and private sector setting aside mandatory contributions during an employee’s tenure. Moreover, the robust governance structure around the national pension system in the UAE afforded it a strong ranking in terms of integrity.

Commenting on the results, Hazem Abdel-Rahman, Mercer’s Retirement Business Leader for the Middle East, stated: “The UAE has a robust pension system in place for Emiratis, which is highlighted by its entry into our annual MCGPI survey ranking alongside many peers that have more established systems. It is notable that the UAE’s retirement benefits are well governed and provide a sufficient income to pension recipients. With that said, as life expectancy continues to rise, the UAE may benefit from increasing the retirement age; this is a step many countries have already taken to ensure the ability to provide for aging and future generations. Furthermore, introducing private pension plans as a complementary retirement program will reduce the pressure on the social security programs in the country and enhance the overall retirement income.”

While the UAE ranks alongside global peers the report has identified a few key areas that require development in the country’s pension system, including introducing a minimum access age to an individual’s retirement benefit, and increasing the state pension age in response to the country’s life expectancy.

“The UAE claiming a place in the top 22 ranking globally testifies the UAE Government’s commitment to ensuring long-term financial planning and well-being for its citizens,” said William Tohme, CFA, Senior Regional Head of Middle East and Northern Africa (MENA) at CFA Institute. “The concerted efforts by the UAE Government over the past few years demonstrate a robust pension system in place in the country which is underpinned by strong governance and international best practices. We are confident that the recently launched ‘UAE Next 50’ initiative, premised on socio-economic transformation, will further act as a catalyst for pension reforms both in public and private sectors. In order for the UAE to improve they need to implement reforms and more compensation measures to incentivise its pension system to balance its aging and retirement ratio. At CFA Institute, we look forward to continue our engagement and collaboration with policymakers and key stakeholders representing the UAE Inc.”

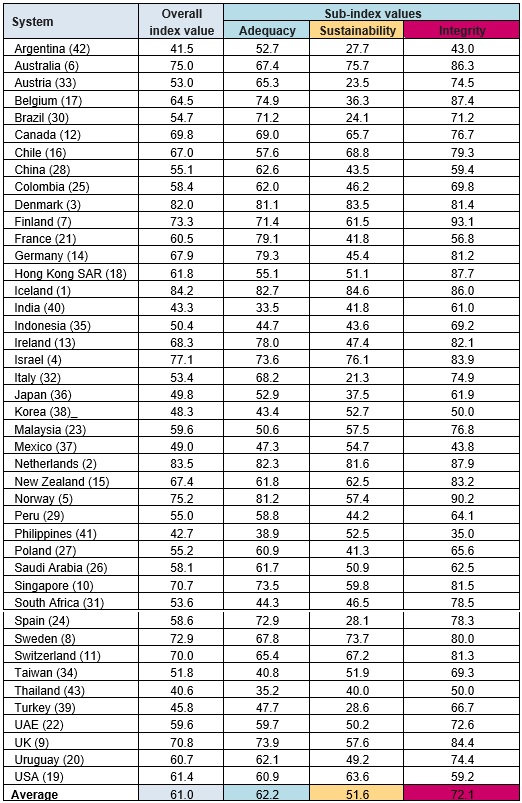

By the numbers

The UAE had an overall index score of 59.6, ranking 22nd on the list. The Index uses a weighted average of the sub-indices of adequacy, sustainability and integrity, and the country demonstrated positive results across all.

The country scored 59.7 in adequacy, due to the generous retirement benefits with suitable minimum pensions relative to earnings. Driven by the labor force participation rate, especially for individuals over the age of 55, the country scored 50.2 in sustainability. The score in this sub-index was bolstered by the sound structure of a funded pension system with mandatory contributions set aside for retirement benefits. The country scored the highest, 72.6, in integrity, owing to the strong governance structure around the pension system.

Global Results

Globally, Iceland had the highest overall index value (84.2), closely followed by the Netherlands (83.5). Thailand had the lowest index value (40.6). For each sub-index, the systems with the highest values were Iceland for adequacy (82.7), Iceland for sustainability (84.6) and Finland for integrity (93.1). The systems with the lowest values across the sub-indices were India for adequacy (33.5), Italy for sustainability (21.3) and the Philippines for integrity (35.0).

In comparison to 2020, China and the UK showed the most improvement as a result of significant pension reform, which improved outcomes for individuals and pension regulation.

2021 Mercer CFA Institute Global Pension Index